Proof of income is a crucial document that is often requested in different instances. It provides a way to validate the financial status of an individual, like proof of their ability to earn.

So, why is this document important?

This article explains more in-depth why proof of income documents are essential, their types, and how to get one. Keep reading.

Proof of Income: An Overview

As seen above, proof of income is a way to show how much money you make. For institutions, it’s a safeguard against fraud, which is a big concern nowadays.

In fact, according to the FTC, Americans admitted to losing an estimated $8.8 billion to scams in 2022. Investment scams accounted for the most significant chunk of that figure, causing over $3.8 billion in losses.

Given these startling figures, the alarming numbers are precisely why institutions often ask for proof of income. It’s not that they don’t trust you; they’re just being careful. And this caution is good for you, too.

After all, by showing proof of income, you’re saying, “I’m real, and my money is real.” This helps you get that deal you need.

Types of Proof of Income Documents

Now, let’s look at the documents themselves. Here are the most commonly requested documents whenever verification is needed.

1. Pay Stubs

A pay stub is a vital document serving as proof of income. It accompanies your paycheck, displaying your earnings and deductions.

It’s pretty detailed, including:

- Gross Pay (Your total earnings before any deductions)

- Net Pay (What you get after all the deductions)

- Deductions (Money taken out for taxes, health insurance, and retirement savings)

- Year-to-Date Totals (The total amount you’ve earned and had taken out over the year)

To put it simply, each time you get paid, your boss writes down how much you earned. They write based on how many hours you work and how much you get paid per hour. Then, they subtract any taxes, insurance fees, the money you put into retirement plans, etc.

The result?

What’s left is your ‘take-home’ pay, the money you get to keep. All of this is shown neatly on the pay stub.

Here’s an example of what a pay stub looks like.

| Employee Information | Details |

| Employee Name | Kevin Wasonga |

| Employee ID | K7891011 |

| Position | Marketing Coordinator |

| Pay Period | 01/01/2024 – 1/15/2024 |

| Pay Date | 01/16/2024 |

| Earnings | Hours | Rate | Amount |

| Base Salary | N/A | N/A | $2,500 |

| Overtime | 8 | $45/hr | $360 |

| Total Earnings | $2,860 |

| Deductions | Amount |

| Federal Income Tax | -$430 |

| State Income Tax | -$110 |

| Social Security Tax | -$178 |

| Medicare Tax | -$42 |

| Health Insurance Premium | -$75 |

| Retirement Plan (401k) | -$143 |

| Total Deductions | -$978 |

| Net Pay | Amount |

| $1,882 |

| Year-to-Date Totals | Amount |

| Gross Earnings | $5,000 |

| Total Deductions | -$1,956 |

| Net Pay | $3,044 |

But what if you’re not traditionally employed? There are other documents like bank statements to validate your income.

2. Bank Statements

These statements record the flow of your money, tracking down all the credits and debits. They are a valid way of income verification as they show the transactions performed in real-time.

For lenders and landlords, your bank statements reflect how you wield money. They can check if you receive your salary on time and manage your expenses well. It’s essential, especially if you have different ways of making money.

Consider this scenario:

Let’s say you work as a freelance web developer. In the past three months:

- You received $3,000 from Client A for a project you finished.

- You also receive $1,500 every two weeks from Client B for ongoing work.

- You pay $1,200 for rent each month and are always on time.

Your bank statement will show that you receive money from different clients monthly, earning a steady income. It will also show that you pay your rent and utilities on time and spend your money wisely.

This fact is significant since it helps demonstrate that you are a person who can be trusted with money in the long run.

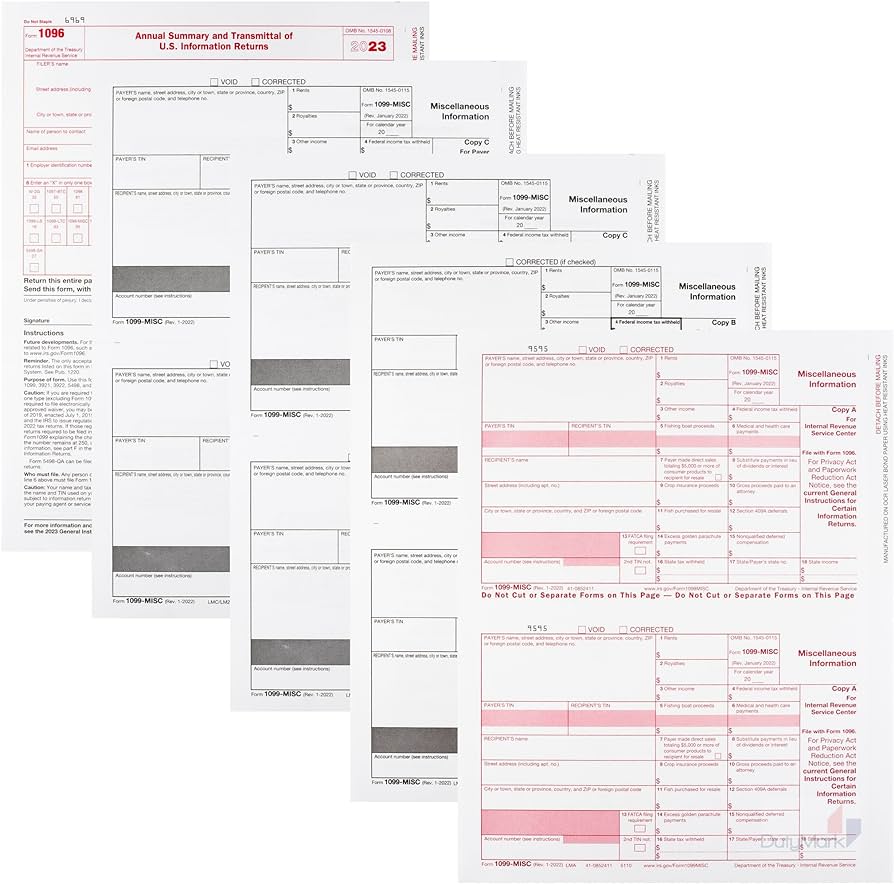

3. W-2 or 1099-MISC forms

W-2 or 1099 are tax forms, another great verification document. These forms are pretty simple.

W-2 forms appear in your mailbox once a year, right from the employer’s end. They are a summarization of the income and taxes deducted from your wages. Think of it as an overall picture of your annual income statement.

It includes salary and withholdings, such as federals and retirement savings plans.

On the other hand, If you’re your own boss or do freelance work, you’ll likely see a 1099-NEC form. This one tallies up what you’ve made on your own steam – from gigs, contracts, and the like. It’s less about taxes taken out and more about reporting your total haul for the year.

Either option can help you prove your income!

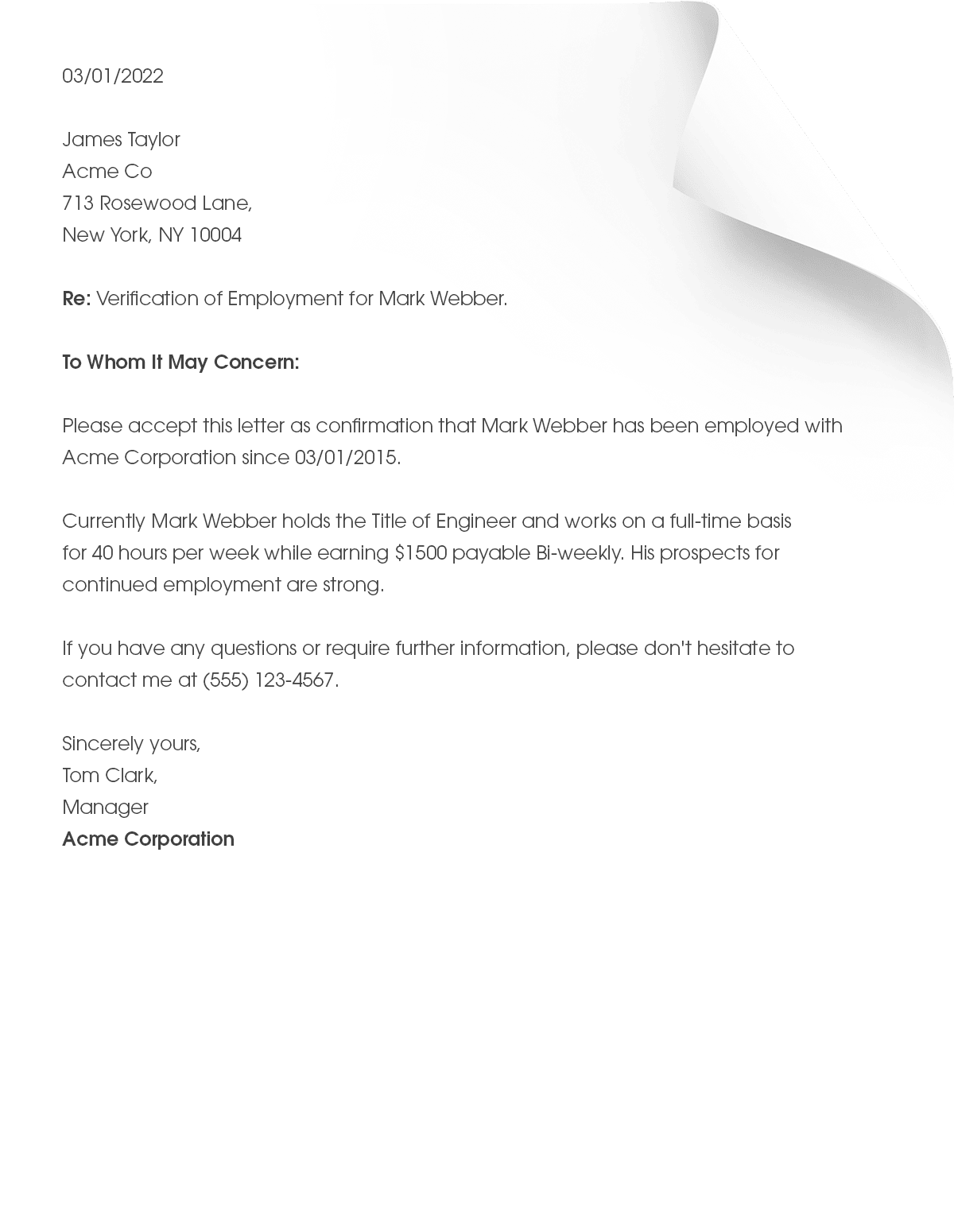

4. Employment Verification Letters

Then, there’s the formal approach: This is a paper from employers confirming if someone works for them, as seen below.

People use it to show how much they earn when they need loans or want to rent a place, and sometimes when background checks are necessary.

The letter usually has the worker’s name, job title, salary, and how long they’ve worked there. It might also say what the person does at their job, but only if it matters why they need the letter.

5. Tax Returns

Lastly, we have tax returns.

It could be your best bet if the above documents don’t match what you have. They are official documents filed by individuals and businesses with the government. Tax returns report income, expenses, and other important financial details.

These documents help calculate tax liability and ensure the right amount of tax is paid.

Here’s a simple explanation:

When you file a tax return, you summarize your financial activity over the past year to the IRS. This includes your total income from all sources and any deductions or credits you’re eligible for. It also has the amount of tax you’ve already paid throughout the year, often through withholding from your paycheck.

Like employment verification letters and pay stubs, they are solid proof of income. But, when you look at your tax return, it only shows how much money you made in the year before. It doesn’t show if you’re working or where your money is coming from now.

This could be seen as a disadvantage.

Situations Requiring Proof of Income

Knowing when and why you may be required to show proof of income will help you with many financial and employment-related processes.

Here are some everyday situations where proof of income is required:

1. Renting an Apartment or House

Leasing offices typically require proof of stable income to ensure you can afford the rent. It serves to verify the creditworthiness of the applicant.

2. Applying for a Loan or Mortgage

Lenders need income documents to evaluate your creditworthiness. It is a requirement of risk determination for lenders.

3. Securing a Credit Card

The lenders may ask you to submit proof of income to secure a credit limit and that you can afford to make the payments.

4. Employment Verification for Job Applications

During job interviews, employers might want proof of your past work. They might ask for a letter from your old boss to check how well you earned money and decide what they can pay you.

Whether it’s a landlord, lender, or employer, they all use credit reports to decide. They look at your credit history and how much you earn now.

How to Obtain Proof of Income

Let’s wrap this up with how you can get these documents. Proof of income can be obtained in different ways. One option is to ask your employer for a letter confirming your income. This is a popular and convincing method.

Alternatively, If you are self-employed, you could write a self-verified letter. However, it is advisable to have it endorsed by a third party, perhaps a CPA.

Moreover, Tax returns and bank statements are the other most reliable documents that can be used as proof of income for self-employed individuals.

But here’s a tip.

Even though these methods have proved effective, Paystub Hero provides a simplified and quick way to create proof of income letters. With Paystub Hero, you can easily make professional pay stubs, a reliable source of income verification.

Experience the Paystub Hero Advantage!

There’s never been an easy way to prove your income until now. Paystub Hero changes that with a simple online service for creating pay stubs, W-2s, and 1099 forms. It’s perfect for anyone needing to show proof of income for apartments, loans, or insurance.

With Paystub Hero, you get accurate, professional-looking documents fast. And if you have any questions, our team is ready to help anytime. Plus, it’s affordable.

So why wait?

Try Paystub Hero and make your income documents today.

Frequently Asked Questions (FAQs)

What is proof of income?

Proof of income is a document or set of documents that demonstrates an individual’s ability to earn. It’s often requested by institutions for financial verification purposes to validate the financial status of an individual.

Why is proof of income important?

Proof of income is essential because it acts as a safeguard against fraud, helping institutions verify an individual’s financial status. This verification process is crucial given the substantial losses to scams reported annually, ensuring that transactions are legitimate and that individuals have the financial capacity they claim to have.

What are the common types of proof of income documents?

The most commonly requested proof of income documents include pay stubs, bank statements, tax forms (W-2 or 1099-MISC), employment verification letters, and tax returns. Each serves a unique purpose in demonstrating an individual’s earnings and financial transactions.

How can pay stubs serve as proof of income?

Pay stubs detail an employee’s gross pay, net pay, and deductions, such as taxes, health insurance, and retirement savings. They provide a clear breakdown of earnings and deductions for a specific pay period, showcasing an individual’s steady income source.